How Money Really Works

Part 2: The Definitive Guide to Credit, Debt & the Illusion of Scarcity — The Money Trick: How Banks Captured the Ledger

Audio read by the author in standard and faster-paced versions:

“Money has become the life-blood of the community… The monetary system is the distributory mechanism.” — Frederick Soddy

If corporations captured the Earth’s resources, banks captured something even more fundamental: the power to measure and control access to them. They did so with one of the most misunderstood inventions in human history: Money.

The Trick

Most people imagine money as a thing. This is understandable. It’s easier to think about owning real things than abstractions. But money is not a thing. Money is credit. A number on a ledger. An accounting entry that tracks claims on society’s resources.

That’s it. That’s all it ever was.

It’s not valuable in itself. It’s valuable as a unit of exchange for things of real value. It’s pure accounting for coordination. It’s just information.

In Part 1, we saw how corporations enclosed the commons, privatizing Earth’s resources and turning collective abundance into scarce property. That was the first capture.

This is the second: banks didn’t just capture money. They captured the very system we use to measure, coordinate, and distribute access to those enclosed resources.

Everything becomes much clearer once you understand this.

How Credit Actually Works (And Who Controls It)

All modern money falls into exactly two categories. Everything else is just an asset.

Permanent (base) credit - Created by governments. No debt obligation. Circulates until deleted through taxation.

Temporary credit - Created by banks. Borrowed into existence. Must be repaid with interest. Disappears when repaid.

Crypto advocates might object here. But digital tokens aren’t money, they’re speculative abstract assets you trade for money.

As we explored in Part 1: “Nations have the power to create money: real credit that requires no repayment. They are monetary sovereigns, the source of the currency itself. But this power is carefully hidden behind an elaborate theatrical performance designed to make money seem scarce, borrowed, or dependent on savings.”

This theatrical performance is what we’re about to dissect.

Governments can, and do, create credit money at will. When a central bank spends into the economy, it doesn’t borrow from anyone. It marks up numbers on a ledger. The credit exists because the government says it exists.

But how does this actually work? Let’s trace the exact flow.

How Permanent Credit Actually Flows

Step 1: Congress Authorizes Spending

Credit is a creature of law, so Congress doesn’t need to “find” money. It authorizes the creation of money through spending bills.

If Congress spends (adds) $7 trillion for the year and collects (deletes) $5 trillion in revenue (mostly via taxes), that’s +$2 trillion permanent credit into the economy. This is usually called the “deficit”, and you’ll see why soon.

Step 2: The Treasury General Account (TGA)

The U.S. Treasury has one main account at the Federal Reserve: the Treasury General Account. This is the government’s checking account. Not at a commercial bank, but at the Fed itself. Really it’s just an accounting entry, mostly for political reasons.

Nations do not “possess” or “save” their own money… they command issuance.

Think of the board game Monopoly. The “bank” in the game works exactly like a sovereign currency-issuing government. The money sitting in the bank box isn’t “in play” yet, it’s just paper waiting to be issued. Players don’t worry about whether the bank “has enough money.” If the bank runs low on bills, you just add more scraps of paper or adjust the numbers. The constraint isn’t the physical bills: it’s the game rules and what players agree to accept.

The Treasury account works the same way. Money sitting there isn’t counted as part of the money supply yet because it hasn’t been spent into the economy. And just like Monopoly, there’s no real limit. The government creates money digitally—just numbers in computers. Those digital dollars can be exchanged for physical bills (Federal Reserve Notes) if needed, but the bills are just tokens representing the numbers. It’s digital numbers all the way down. Pure accounting.

In Monopoly, everyone knows the bank can’t run out. In real life, we’ve been deceived to believe the opposite.

Step 3: Taxes Flow In

You can think of taxes as either:

Money recycled back into the Treasury account, or

Money deleted and then recreated when spent

Either framing works since the balances are identical. Taxes delete money. They don’t “fund” anything! They simply remove money from circulation.

Step 4: Treasury Issues Bonds

Operationally, current law requires Treasury to issue bonds essentially equal to the “deficit”, but this is a self-imposed rule, not a funding necessity.

That +$2 trillion now sitting in bank accounts represents potential spending power. If it flows into consumption or investment too quickly, it drives up prices. So bonds drain the $2T by converting spendable deposits into locked-up savings that earn interest but can’t immediately bid up prices.

When you buy a Treasury bond, you’re transferring liquid deposits from your bank into a time-locked interest-bearing account at the Fed. The same way your bank considers your deposit their liability, the Fed too records these as a liability and calls it “debt.”

It’s crucial to know these bonds are not borrowing in any real sense.

The money doesn’t leave the economy. It’s still there, but locked into a bond, sitting on someone’s balance sheet as an asset, earning interest. It’s in the game. Just temporarily parked.

So why issue bonds at all? Three reasons:

Drain money from the banking system to manage interest rates & inflation

Create safe assets for wealth storage with guaranteed interest

Shape the illusion that government spending is “financed” by savings

In other words, the banking cartel gaslights the public so it can collect guaranteed interest directly from government.

Step 5: The Fed Credits the Treasury

Most people think when taxes are paid and bonds are sold, the proceeds flow into the TGA and fund spending. What's actually happening is different. Taxes deleted money. The bond money is still in the game, just parked. The Fed credits the TGA with those amounts. That’s it. The Fed is the government’s bank, not a constraint on it.

The key insight: Money is created by keystrokes. Money is deleted by reverse keystrokes. Debt is an illusion at the sovereign level.

Step 6: Treasury Spends

The Fed processes every payment when the government pays contractors, employees, or Social Security recipients:

Treasury instructs the Fed to make payment

Fed debits the Treasury account

Fed credits the recipient’s bank’s reserve account

The bank credits the recipient’s deposit account

Now the money is “in the game.” It’s circulating in the economy.

The “National Debt”

What we call the national debt is simply the accumulation of all those bonds: time-locked savings accounts at the Fed.

It’s not debt in the household sense. It’s the record of:

How much permanent credit the government has created

Minus how much it has taxed back

Held in interest-bearing form by bondholders

The government pays interest on these bonds. But the government creates the money to pay the interest. It’s a circular flow designed to provide guaranteed income to bondholders: wealthy individuals, funds, banks, and foreign governments.

Why Don’t Nations Save Their Own Currency?

A government that creates dollars doesn’t need to save dollars. That would be like the Monopoly bank “saving” money in separate piles.

Real savings for a nation would be:

Real capital (infrastructure, technology, educated workforce)

Foreign currency reserves (for international trade)

Strategic resources and other assets

But saving your own currency, numbers that you create on demand, is beyond absurd. Yet we’re told governments must “save” or “borrow” to spend. The theatrical performance continues.

Reserves: The Base Money

When the Fed credits the Treasury account and then settles Treasury payments, it creates what it calls reserves: the base layer of money in the system.

Reserves are 100% digital numbers:

Held only by banks (individuals cannot hold reserves)

Used to settle payments between banks

Created and deleted by the Fed

Permanent credit (until taxed back or drained through bond sales)

Nations that issue their own currency cannot “run out of money”. The constraint is never money… it’s real resources, inflation, and political will. But never money itself because numbers are infinite.

Taxes don’t fund government spending. This is perhaps the hardest myth to kill. Taxes regulate demand, create a need for the currency, and reclaim some of what was created. The government creates money first, then taxes it back. Not the other way around.

This would be obvious if we thought about it for ten seconds. But we don’t. We prefer the household budget metaphor. It’s comforting. It’s wrong. But it’s comforting.

Reserves are "base" money. Next: how temporary credit — bank money — is created on top of this permanent base.

How Banks Create Money

Most money creation has been legally mandated to private banks.

Here’s how it works: You want a $300,000 mortgage. You go to a bank. The bank does not check its vault. It does not gather deposits. It does not call other customers to see if they’d like to lend you their savings.

Instead, the bank opens a spreadsheet. It types “$300,000” next to your name.

That’s it.

New money now exists. Money that, thirty seconds earlier, did not exist anywhere in the universe.

The bank created a liability (your deposit), which you’ll use to buy a house. And it created an asset (your contract to repay), which it considers valuable enough to hold on its books. This is called double entry bookkeeping.

The bank created this money at zero cost. It gave up nothing. It sacrificed nothing. It produces purchasing power out of nothing, and now you owe it back… with interest.

They call this lending, but it’s really alchemy with collateral.

When people say “banks lend out deposits,” they are describing a fairy tale. Banks create deposits when they make loans. The loans come first. The deposits follow.

The Bank of England confirmed this in 2014. The Bundesbank confirmed it. The Federal Reserve has confirmed it. Every major central bank now admits: banks create money when they lend.

And yet, somehow, the myth persists. Perhaps because the truth is too unsettling.

“The process by which banks create money is so simple that the mind is repelled. With something so important, a deeper mystery seems only decent.” John Kenneth Galbraith in Money.

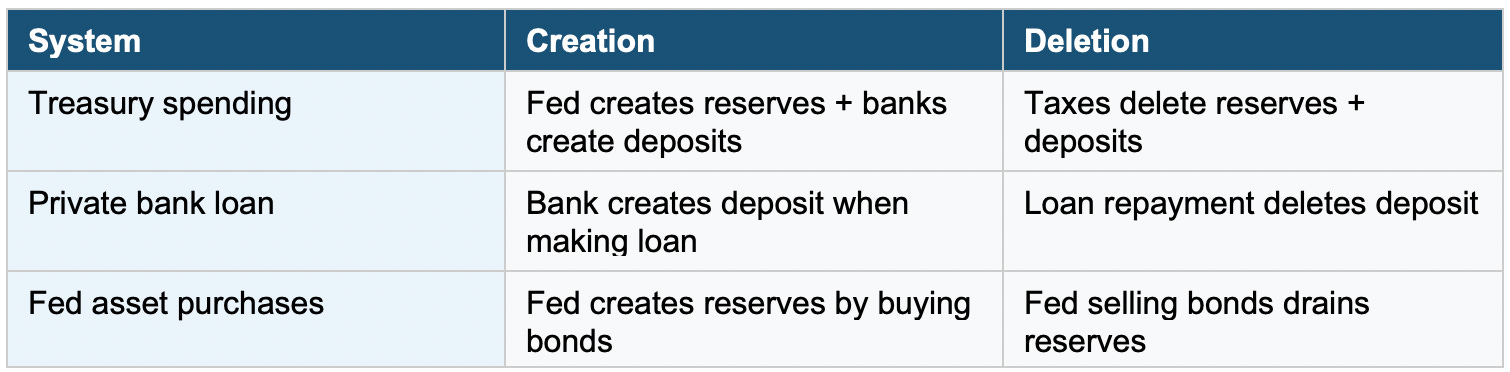

Comparing Money Creation and Deletion

The Power Worth Fighting For

This power to create credit—who controls it and under what terms—has always been worth fighting for.

The American Revolution was sparked by exactly this issue.

In 1765, the British Crown banned the American colonists from banking, from issuing their own colonial credit. Instead, colonists were forced to conduct all trade in gold coin which was scarce, taxed away, and shipped back to Britain.

The colonial economy collapsed. Not because the colonists became lazy or incompetent, but because they’d been cut off from the means of exchange. Credit dried up. Trade ground to a halt. Prosperity turned to poverty.

The famous Boston Tea Party wasn’t just about tea, it was about taxes draining away the gold they needed to trade, while being forbidden from creating their own credit to replace it. Benjamin Franklin later wrote that the restriction on colonial credit was the deeper cause of the Revolution.

The Revolution was many things. But economically, it was a war over who gets to create credit.

To win the war, the colonists borrowed gold from France and crucially began issuing their own credit again called Continental currency. They seized back the power to create money.

That war never really ended. It just moved from battlefields to political bank charters, from kings to central banks, from overt control to legal systemic design.

The question remains: who should have the power to create the credit that mobilizes society’s real resources and either enables life or restricts it?

Right now, the international banking cartels have captured that power. And as we’ll see, that choice has consequences.

Let’s Start a Bank

To understand what banks really are, let’s become one.

But first, a comparison. Because understanding what makes banks special requires seeing what normal companies do and what banks do differently.

If You Start a Normal Company: You file paperwork to get a tax ID and become a legal person who can open a bank account. After you raise capital you can hire people, buy things, and sell things. Now you’re playing the great game of capitalism.

If You Want to Start a Bank: Completely different rules.

But before we walk through the steps, here’s something important to understand: our bank operates as two separate businesses under one roof.

Business #1: Credit Creation (Making Money) When the bank issues a loan, it does not transfer existing deposits. It creates a new deposit. The money did not previously exist. We grow the money supply.

Business #2: Custody & Settlement (Moving Money) The bank holds deposits, processes payments, clears checks, settles transfers between banks, and manages reserves. We manage existing money as a financial utility.

The first business manufactures money. The second business moves it. They operate together, under the same roof, but they are fundamentally different powers.

Step 1: Get a Charter

You need a banking charter. Not a business license. Regulators want to know: Do you have enough capital? Do you understand risk management? Can you operate safely inside the payments system?

If approved, you’re in. You’re now a member of the Federal Reserve System.

Step 2: Raise Capital

Let’s say we need $1 billion. Investors put up real money. That billion becomes our bank’s capital, our equity, our skin in the game.

Here’s where it gets interesting.

Step 3: Join the Fed (Central Bank)

With our charter and capital, we must now purchase stock in one of twelve regional Federal Reserve Banks. If we’re in New York, we buy into the New York Fed. San Francisco? The San Francisco Fed.

This isn’t optional. It’s required. We pay less than 1% of our capital to own shares in the regional Fed.

What do we get for this? On that paid-in capital stock, the Fed pays a statutory dividend (historically 6%, now capped at the lesser of 6% or the 10-year Treasury rate for the largest banks). It’s not tradeable stock. It doesn’t control the Fed directly. But it is a guaranteed return on capital.

Step 4: Open Our Reserve Account

Now we deposit our billion at the Fed. This creates our reserve account, our savings account at the Federal Reserve. Every customer deposit we take in also flows into this account. This is the operational heartbeat of the bank. Every payment in, every payment out, every settlement between banks flows through here.

Every digital dollar you deposit sits in our reserve account at the Fed. The Fed pays us interest on it called IORB, currently 3.65%, as high as 5.4% in 2024. Not you. Us.

And who sets that interest rate? The Fed does. The same institution owned in part by the banks collecting it.

How much do we pay customers? As little as possible of course. Presently less than 1%. Because regulation is largely written by the industry, enforced by former insiders, and structured around bank profitability. Who do you think shaped the rules on banking in most countries?

Step 5: Get Deposit Insurance

Before we can accept customer deposits, we buy insurance from the FDIC at less than 0.1% of our deposits. The FDIC guarantees that if we lose more than our capital can cover, depositors won’t lose their savings.

This is the foundation of public trust. Customers don’t worry about whether their money is safe. They assume it is. The FDIC made that assumption permanent.

Step 6: Operating the Bank

We also have a checking account… with ourselves. That’s right: we are our first customer. When we pay salaries, rent, dividends, we transfer money from our reserve account at the Fed into our own commercial checking account, and then spend it.

When customers deposit money, it goes into our reserve account, earning us interest. When customers withdraw money or write checks, we transfer reserves to other banks to settle the payment.

When a customer wants physical cash, we swap our reserves (earning 3.65% at the Fed) for bills and coins (earning nothing). Cash just sits in our vault, dead weight.

This is why banks restrict cash withdrawals and require advance notice for large transactions. It’s not about security. It’s about interest. When your money sits as reserves at the Fed, we profit. When you take it as cash, we don’t.

Excess cash? Swapped back to the Fed for reserves immediately. The system is designed to keep your money digital, where it earns us passive income. Most proposed stablecoin legislation would require stablecoin issuers to hold reserves at banks. It’s marketed as “safety,” but look closer: it’s another mechanism to push more deposits into the banking system, earning us more interest on reserves.

Step 7: The Magic Part

But here’s what makes banking special:

We don’t need to use deposits to make loans.

We can make up to $20 billion in loans against that $1 billion in capital.

How? We create new deposits. We don’t lend out existing money. We create it.

A customer wants a $500,000 mortgage. We simply type “$500,000” into the customer’s account. New money. Created by us.

On our books:

Asset: $500,000 mortgage contract (the customer’s promise to repay)

Liability: $500,000 deposit (the customer’s account balance)

The customer buys the house. That $500,000 moves to another bank. Our reserves drop by $500,000 to settle the payment. But we still have the $500,000 mortgage as an asset, and the customer still owes us $500,000 plus interest.

And here’s the crucial distinction: we created that $500,000 deposit out of nothing. But we cannot create reserves. Only the Fed can do that.

If we run low on reserves, we borrow them overnight from other banks (through the federal funds market) or from the Fed itself. Reserves are just for settling payments between banks. They’re not the constraint on lending.

The constraint is capital: our required equity relative to the loans we make. As long as we maintain proper capital ratios as per the Bank of International Settlement (BIS.org), we can keep creating new money through lending.

Step 8: The Returns

So let’s tally what we get for our $1 billion:

6% guaranteed dividend from our Fed stock ownership

Interest on reserves: roughly 3.65% on all deposits sitting at the Fed

Interest on loans: typically 5-8% on the $20 billion in loans we can create

Fees: loan fees, overdraft fees, account fees, wire transfer fees, ATM fees

The returns on our original $1 billion are extraordinary. We’re earning a dividend on the capital we were required to invest, interest on the reserves that your deposits generate, and interest on the $20 billion in new money we created from nothing. The original billion just sits there, quietly collecting. All of it guaranteed.

The System

Now multiply this by every bank in America. Thousands of them. All creating money through lending. All collecting interest on reserves. All receiving guaranteed dividends.

And the Fed itself? It holds over $7 trillion in government bonds, purchased with money it created. It collects interest from the U.S. government on those bonds. It pays interest to banks. It pays dividends to member banks. And then, if there’s anything left, it sends the remainder to the Treasury.

Since 2022, there’s been nothing left. Interest rates rose. The Fed now pays banks more in interest than it earns from its bond holdings. Instead of going bankrupt, it books a “deferred asset” (an accounting IOU to itself) and continues operating.

An institution that creates money cannot go broke. It can only create more money.

Now you understand what a bank is. It’s not a building or a vault. It’s a license to create money, backed by membership in a private cartel that owns the Federal Reserve System.

The Price of Everything

Here’s something most people never think about:

Every price you pay contains layers of tribute to ownership positions.

When you buy a loaf of bread, you’re not just paying for wheat, labor, and energy. You’re paying:

Interest on the bakery’s business loan

Rent on the bakery’s leased property

Interest on the farmer’s equipment loans

Rent on the farmland (to absentee landowners)

Royalties on patented seeds (to agribusiness monopolies)

The resource toll on every input extracted from land owned by someone who did nothing but hold title

Interest on the trucking company’s vehicle financing

Executive salaries, bonuses, travel, dining, club memberships, and corporate perks at every company in the chain

Profit to shareholders at every stage of the supply chain

Taxes embedded in every business cost, marked up and passed straight to you

At every single stage of production, someone is extracting value simply for owning something: not for doing anything, not for creating anything, but for having captured a strategic position in the production chain.

These aren’t market prices reflecting real costs. These are tribute payments embedded in the price structure itself.

And what made all of this extraction possible? The power to create credit and the choice to issue it only as debt.

At every stage, someone created money as debt and now extracts tribute forever.

The debt IS the money. The system doesn’t just allow extraction... it requires it! The tribute is baked into every transaction.

You’re not buying bread. You’re paying interest to banks and rent to a dozen different landlords, and the bread is just the excuse for those transfers.

The Mathematical Trap

When a bank creates $100,000 for your loan at 5% interest, it creates $100,000 in new deposits. But you owe $105,000.

Where does the extra $5,000 come from?

It doesn’t exist yet.

It must come from income earned somewhere else in the system: new lending, government deficit spending, or banks recycling their interest income back into circulation.

The system doesn’t make repayment impossible. But it does make continuous expansion structurally necessary.

At any point in time, the system requires continual new lending or redistribution to service interest, otherwise defaults rise. Someone must fail. Someone must default. The system requires it.

This is why the system demands perpetual growth. Without constant new loans, existing debts cannot be serviced. Without expansion, there is collapse.

When you repay a loan, the principal disappears. The bank’s asset and its liability both vanish. Money is destroyed.

But the interest you paid? That stays. That’s the bank’s profit. That’s real.

So the money supply shrinks every time loans are repaid… unless new loans are made to replace them. Scarcity is not accidental. It is engineered into the base code of the system.

Galbraith called this “the innocent fraud.” Innocent because everyone participates without realizing what they’re doing. Fraud because it is, nonetheless, a fraud.

The Scarcity Story

We are told there is not enough money.

Not enough for healthcare. Not enough for education. Not enough for infrastructure, housing, clean water, or preventing ecological collapse.

We are told the government must tax before it can spend. That it must borrow what it cannot tax. That deficits are dangerous. That we cannot “afford” things.

This is, to be technical about it, horseshit.

The government creates money. It cannot run out. It faces no budget constraint in its own currency.

What we call the “national debt” is the cumulative total of dollars spent into existence minus the dollars taxed back out. The bonds issued to “finance” this gap are just interest-bearing savings accounts at the Fed. The “debt” is actually the money supply.

When someone says the U.S. “owes” $36 trillion, they are saying: the government has created $36 trillion more than it has destroyed through taxation, and it pays interest to those holding that wealth in bond form.

The government doesn’t issue bonds because it needs money. It issues them to give banks, corporations, and wealthy individuals a place to park dollars and earn interest. It’s a subsidy to wealth, dressed up as fiscal necessity.

The constraints on government spending are real, but they are not financial:

Real resources - Can we actually produce the thing?

Labor - Are people available to do the work?

Inflation - Will spending push prices up?

These are economic questions. Important ones. But they are not questions about money. Money is just numbers on the ledger. We can always add to the ledger.

A world where people starve, freeze, and die of preventable disease—not because there isn’t enough food, shelter, and medicine, but because we refuse to update the ledger—is a world that has chosen mass death for accounting reasons.

Scarcity is a political choice. Not an economic fact.

Who Benefits?

The system is not an accident. It was designed. By bankers. For bankers.

Banks benefit because they create money as debt and collect interest on it forever. They are gatekeepers to the money supply, extracting rent from every economic transaction.

Existing wealth-holders benefit because scarcity narratives prevent redistribution. If the government “can’t afford” social programs, existing wealth remains unthreatened.

When everyone believes money is scarce, any government spending becomes a zero-sum game: “If we spend on healthcare, we can’t spend on infrastructure” or “If we help the poor, we must take from someone else.”

This frames all policy as trade-offs between competing interests, leading to gridlock and status quo preservation.

But it’s deeper than that. When government spending employs people, it tightens labor markets. Workers gain bargaining power. Wages rise. Rising wages mean workers capture more of the economic pie. But wealth-holders don’t just want to be rich, they want to be relatively richer than workers. Scarcity narratives prevent that shift.

Creditors benefit because debt must be repaid in full, while inflation erodes its value. Creditors prefer tight money, high interest rates, austerity, and unemployment. Anything that protects their nominal debt claims.

Workers lose because unemployment is deliberately maintained to prevent wage growth. The Fed raises rates explicitly to slow hiring. They say this openly. “Cooling the labor market” means “keeping workers desperate.”

Debtors lose because they pay interest on money created at zero cost. The asymmetry is total.

This is not a moral judgment. This is description. The system works exactly as designed. For some people.

The Inflation Bogeyman

“But won’t printing money cause inflation?”

Maybe. Maybe not. Depends.

Japan ran massive deficits for three decades. Result? Deflation. The U.S. tripled the monetary base after 2008. Result? Barely any inflation. The Fed created trillions during COVID. Result? Inflation, yes, but mostly in assets that rich people own and in sectors suffering supply chain disruptions.

Weimar Germany and Zimbabwe had hyperinflation. But they also had collapsed productive capacity, political chaos, and foreign-denominated debts.

Inflation happens when money creation exceeds productive capacity. That’s the rule.

If you create money and use it to employ idle workers building useful things, you get more goods and more money with no inflation. If you create money and people bid for the same limited supply of goods, prices rise.

Bank lending creates inflation when it flows into housing speculation and stock buybacks. Public spending creates value when it flows into infrastructure and education.

Hyperinflation requires systemic collapse, not just money creation. Yet we’re told to fear public investment while ignoring private speculation.

Why? Because the people warning about inflation benefit from scarcity.

Modern Monetary Theory (MMT)

Some economists have formalized this understanding into MMT. It observes:

Currency-issuing governments cannot run out of their own money

Taxes don’t fund spending—they regulate inflation and demand for currency

The real limit is inflation, not deficits

Unemployment is a policy choice, not economic necessity

Bond issuance is about interest rate management, not financing

Critics call this radical. It’s not. It’s description.

MMT doesn’t advocate printing unlimited money. It advocates understanding how money actually works, so we can have honest debates about real resource constraints instead of fake debates about accounting.

The radical thing isn’t MMT. The radical thing is pretending the current system is natural, inevitable, or fair.

Debt as Control

Debt is more than financial. It’s social discipline.

Student debt prevents risk-taking. Can’t quit your job because you have loans. Can’t take time off to care for aging parents because you have loans. Can’t protest, organize, or challenge power because you have loans.

Mortgage debt enforces compliance too. Can’t strike, you have a mortgage. Can’t relocate for better opportunities, you’d lose equity. Can’t reduce hours to spend time with your children, the bank doesn’t care about your children.

Medical debt bankrupts families. In the richest country in human history, people die rationing insulin because updating the ledger is apparently too expensive.

National debt justifies austerity. “We can’t afford it” cuts education, healthcare, infrastructure all while military budgets expand and bank bailouts appear instantly.

The debt IS the money. Without debt, there would be no money. The system requires people to go into debt to access the means of exchange.

This gives extraordinary power to those who control credit creation. They decide who gets money. Who gets opportunity. Who gets to participate in the economy.

It’s not a bug. It’s the core feature.

The Illusion Dissolves

Money is not a thing. It’s a social agreement. A ledger. A claim on resources.

Which means it can be redesigned. We are not trapped in a system of artificial scarcity and compounding debt. We chose this system. We can choose differently.

We can create money as a public utility instead of private profit. We can issue credit without debt. We can update the ledger to reflect our actual values instead of bank balance sheets.

The current system isn’t natural. It’s not inevitable. It’s not even particularly old: this version has only existed since 1971, when Nixon closed the gold window.

We’ve been playing the wrong game.

We’ve been treating money as scarce when it’s abundant. We’ve been competing for credit when we could be coordinating with it. We’ve been measuring wealth by capital accumulation when we should be measuring it by our capacity to care for one another.

This is what Creditism offers: not just a critique, but a blueprint for what comes next. A redesign where credit flows to everyone as a birthright—not as debt, but as guaranteed access to life itself.

Where markets still exist, but survival doesn’t depend on winning them.

Where money is recognized for what it actually is: just information. Just coordination. Just math.

And math can be rewritten. Numbers are infinite. Scarcity is a choice.

Toward Part 3: The Copernican Revolution

Humanity once believed the Earth was at the center of the universe.

Then Copernicus showed us the truth: we orbit the sun. The Earth isn’t the center. It never was. That shift from geocentrism to heliocentrism didn’t just change astronomy. It changed how we understood our place in the cosmos.

We need a similar revolution in economics.

Right now, Capital sits at the center of our economic universe. Everything revolves around it. The entire purpose of our economy is to extract, accumulate, and protect Capital. We compete for it. Kill for it. Structure our entire civilization around acquiring more of it. We measure ourselves by it, our net “worth” determined by how much we’ve captured and hoarded.

Capital is treated as the source of all value: the sun around which everything must orbit.

But what if this is backward?

What if the real source—our economic sun—is Credit?

Not credit as in debt. Credit as in belief. Trust. A shared promise. The capacity to coordinate, invest in one another, and build futures together.

Credit is what money actually is: a social technology for coordination. And just as the sun gives life, credit—properly distributed—could power an economy centered on life itself.

Not on banditry and hoarding. Not on scarcity. But on participation, creativity, and shared security.

Capital is dead weight: accumulated claims on past production. Credit is living energy: the capacity to mobilize resources for future creation.

We’ve been orbiting the wrong center. And it’s killing us.

What Comes Next

In Part 1, we saw how corporations enclosed the commons—turning collective resources into private property, transforming abundance into artificial scarcity.

In Part 2, we’ve seen how banks captured the ledger—turning credit into debt, making access to life conditional on servicing interest payments to those who create money from nothing.

Two captures. Two forms of theft. One system of control.

In Part 3, we’ll explore what it means to reclaim both to build an economy where:

Credit flows as a birthright, not a privilege earned through debt

Resources serve life, not profits

Coordination replaces competition as the organizing principle

Money becomes what it always should have been: a tool for abundance, not a weapon of scarcity

This is Creditism: the economic operating system for a civilization that’s finally learned to live with itself.

Not utopia. Just better design.

Not revolution. Just rewriting the rules.

Not hope. Just math.

The game is rigged. It has always been rigged. But the riggers are not invincible.

They just control the ledger.

For now.

This is Part 2 of 3. Part 1 covered Nations, Corporations, and the First Crime. Part 3 will explore Creditism: the path to economic liberation.

| A guest post by

|

Good work!

Frederick Soddy - To allow it (money) to become a source of revenue to private issuers is to create, first, a secret and illicit arm of the government and, last, a rival power strong enough ultimately to overthrow all other forms of government.

Typo., "The Treasury credits the TGA": You meant, "The Fed credits the TGA."

But note that what you didn't mean is that the Fed credits the TGA using its own account, the Fed Fed account (SOMA).

The sum is but the simple difference between Treasury payments to that bank and that bank's to the Treasury, whichever is greater, so the Fed hasn't *actively* done anything there.